Boosting US productivity represents a $10 trillion opportunity in US GDP between now and 2030

Boosting US productivity represents a $10 trillion opportunity in US GDP between now and 2030

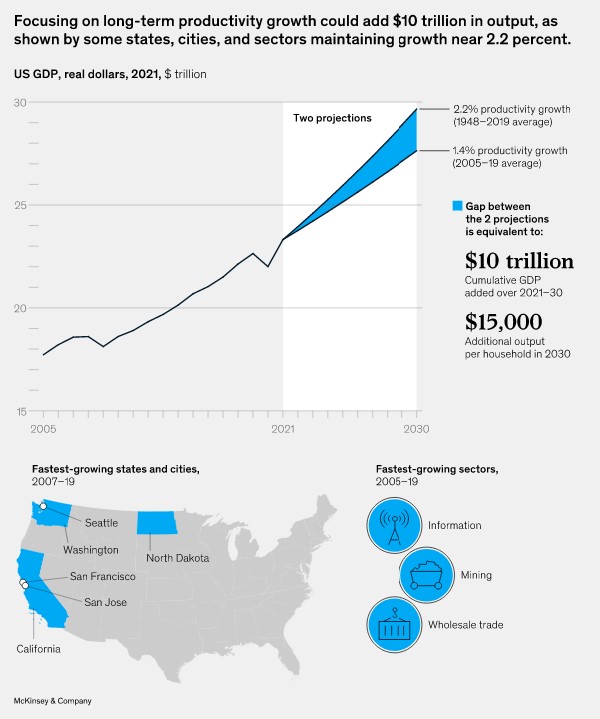

Since 2005, US labor productivity has grown at a lackluster 1.4 percent annually. At the same time, real wages have slowed and workforce participation has declined. Regaining the long-term productivity growth rate of 2.2 percent would help the country confront looming challenges, including workforce shortages, debt, inflation, and the cost of the energy transition.

But if the US economy were a car, the engine has been sputtering for a while. In the past 15 years, productivity growth has averaged just 1.4 percent, even as incredible advances in digital technology put a supercomputer in every pocket. This state of affairs is well known. It is also not confined to the United States. Most OECD countries have seen a drop in labor productivity growth since 2005.

In the US economy, there’s also a problem with the transmission. The link between productivity growth and real incomes has weakened. In the postwar boom from 1948–70, incomes grew at 3.0 percent annually, while productivity growth averaged 2.8 percent. More recently, real incomes have grown at 0.7 percent, well below the 1.4 percent gains in productivity. Worse, not everyone has shared equally in the relatively low gains in income, and labor participation rates have fallen from 67 percent in the 1990s to 63 percent in 2019, as millions have become discouraged about work.

Achieving and equalizing productivity gains will require concerted action.

Priorities include:

- unlocking the power of existing technology,

- investing in intangibles,

- improving workforce reskilling and

- labor mobility, and

- implementing place-based approaches tuned to specific geographies.

– Report: Rekindling US productivity for a new era, February 2023